Would Your Financial Information Stand Up To Scrutiny?

Most businesses feel comfortable with their financial information until somebody important starts relying on it.

- A lender wants to assess affordability.

- An investor wants to understand growth assumptions.

- HMRC asks for supporting evidence.

- A board member wants to understand why cash has moved differently from profit.

Suddenly, the question is no longer: “Do we have the numbers?”

It becomes: “Can we defend the decisions those numbers support?”

That is often where businesses discover the difference between producing financial information and truly understanding it.

Key Takeaways

- Financial scrutiny is usually a test of clarity rather than compliance

- Strong financial information should be explainable, not just reportable

- Inconsistencies create questions that become difficult to answer

- Cash flow often attracts more attention than profit

- Connected forecasting improves confidence in future decisions

- Decision-ready information is easier to trust because it is easier to understand

Why Do Simple Questions Sometimes Become Difficult To Answer?

Most scrutiny starts with relatively straightforward questions.

- Why has revenue changed?

- Why has cash moved differently from profit?

- Why does this forecast differ from the previous one?

None of these are complicated questions.

Yet many businesses struggle to answer them quickly.

The problem is rarely a lack of information. In fact, most businesses have more reports, dashboards, and spreadsheets than ever before.

The issue is that the information often exists in separate places.

- Revenue is reported one way.

- Cash is reviewed somewhere else.

- Forecasts are maintained independently.

When the information is disconnected, every question requires additional explanation.

The numbers may be technically correct.

But they do not immediately tell a coherent story.

What Are Banks, Investors, and HMRC Actually Looking For?

Whether the questions come from a bank, investor, board member, or HMRC, they are usually trying to establish the same thing.

Can the numbers be trusted?

That trust comes from understanding where the information came from, how it was produced, and whether it behaves consistently over time.

The strongest financial information is rarely the most detailed.

It is the easiest to explain.

The same principle applies during formal reviews. HMRC requires businesses to retain accounting records and supporting documentation for at least six years.

The requirement is not simply to hold information. It is to be able to support and explain it when questions arise.

Strong financial information works in exactly the same way. It is built on clarity, consistency, and traceability rather than volume.

What Happens When Financial Information Stops Supporting Decisions?

One of the clearest signs of a weak financial structure is not that the numbers are wrong.

It is that the numbers stop helping the business make decisions confidently.

- The reports still exist.

- The management accounts are still produced.

- The forecasts are still updated.

But every important discussion begins with:

- “Why has this changed?”

- “Which version is correct?”

- “What assumptions are we using?”

- “Can somebody explain this movement?”

Instead of helping decisions move forward, financial information starts creating friction.

Management meetings become discussions about interpreting reports rather than acting on them.

- Investment decisions take longer.

- Forecasts lose credibility.

- Growth opportunities become harder to evaluate.

The issue is rarely a lack of information.

It is that confidence in the information begins to weaken.

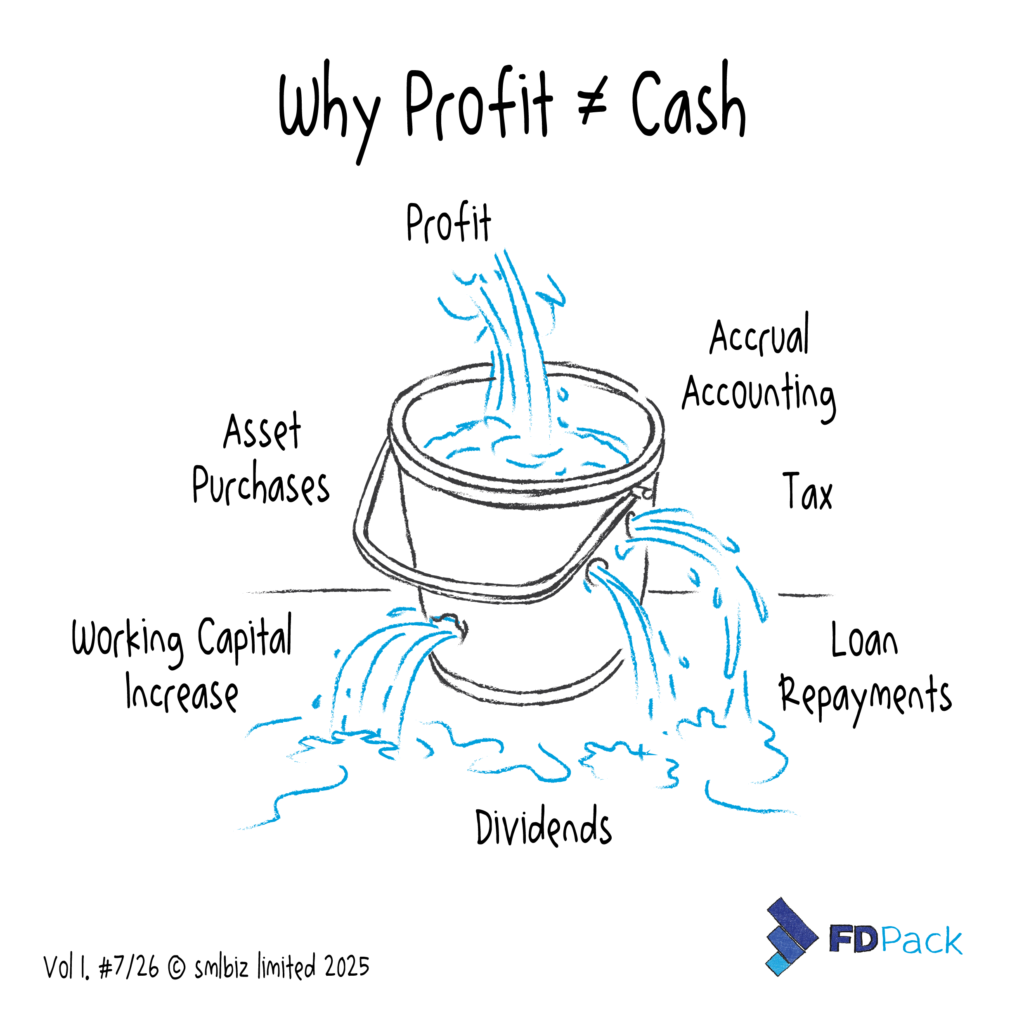

Why Does Cash Usually Attract The Most Questions?

Profit is important. Cash is where scrutiny usually begins.

Because cash is where financial performance becomes operational reality.

A business can report healthy profits while simultaneously experiencing increasing pressure on liquidity.

For example:

- customers may be taking longer to pay

- working capital requirements may be increasing

- future commitments may already be consuming available cash

This is why lenders often spend less time discussing reported profit and more time understanding:

- cash generation

- working capital behaviour

- future obligations

- liquidity resilience

Understanding those relationships is often more important than understanding the profit figure itself.

This is becoming increasingly important in lending discussions.

Recent UK reporting has shown SME loan approval rates have fallen to below 50%, compared with around 67% in 2018. As lenders apply greater scrutiny before extending finance, businesses increasingly need financial information that is not only accurate, but also clear and easy to explain.

The question is rarely whether the numbers exist.

It is whether confidence exists in what those numbers are saying.

Why Does Forecasting Matter When Somebody Starts Asking Questions?

Historical reporting explains what happened.

Most important decisions depend on understanding what happens next. This is where forecasting becomes critical.

A forecast should not exist separately from the rest of the financial information. It should extend naturally from it.

When assumptions change, the reasons should be visible.

When forecasts move, the underlying drivers should be understood.

A forecast that requires constant adjustment or explanation often indicates deeper structural issues within the underlying financial information.

The objective is not forecasting accuracy in isolation.

It is forecasting that reflects how the business actually behaves.

How Do You Build Financial Information That Holds Up Under Scrutiny?

Most scrutiny begins with a simple question.

The challenge is that the answer rarely sits inside a single report.

For example:

- revenue affects debtors

- debtors affect cash flow

- cash flow affects liquidity

- liquidity affects the balance sheet

The numbers are connected.

The financial information should be too.

This is where many businesses struggle.

Reporting may exist across multiple spreadsheets, dashboards, and forecasts, but the relationships between those numbers are not always visible.

When that happens, every question requires additional explanation.

Connected financial information reduces that friction.

This is one reason three-way forecasting has become increasingly valuable for growing businesses.

By linking:

- Profit & Loss

- Cash Flow

- Balance Sheet

into a connected financial structure, businesses can understand not only what has happened, but why it happened and how future decisions may affect the wider financial position.

The result is not simply better forecasting.

It is financial information that becomes easier to support, explain, and trust when questions arise.

Why Does Scrutiny Expose Weak Financial Structures So Quickly?

Scrutiny has a way of revealing issues that remain hidden during normal operations.

A report may appear reliable until somebody asks:

- how was this calculated?

- why has this changed?

- what assumptions are driving this forecast?

- how does this relate to cash flow?

At that point, weaknesses become visible very quickly.

For example:

- assumptions may exist in multiple places

- reports may use different methodologies

- spreadsheets may require manual adjustments

- financial movements may not reconcile consistently

Individually, these issues may seem manageable. Collectively, they reduce confidence in the information.

The problem is not usually that the numbers are incorrect.

It is that explaining them becomes unnecessarily difficult.

The strongest finance functions are not the ones producing the most reports.

They are the ones producing information that remains consistent when somebody starts asking questions.

Confidence Exists Before the Questions Are Asked

At some point, every business faces scrutiny.

It may come from:

- a lender

- an investor

- HMRC

- a board meeting

- or simply the business owner trying to understand what is happening

The businesses that handle those conversations most confidently are rarely the ones with the most reports.

They are the ones with financial information that remains consistent, connected, and explainable when questions arise.

- Assumptions can be traced.

- Movements can be understood.

- Decisions can be supported.

FDPack helps businesses build structured management accounts and connected forecasting that extend directly from actual performance.

Because confidence is not created when somebody asks the question.

It is created long before the question is asked.

FAQs

What does it mean for financial information to stand up to scrutiny?

It means the numbers can be clearly explained, supported, and trusted when questions are asked.

Why is explainability important in financial reporting?

Because confidence comes from understanding where the numbers came from and how they connect to the wider business.

Why does cash flow receive so much attention?

Cash reflects how financial performance translates into operational reality and often highlights issues that profit alone does not reveal.

What is the benefit of 3-way forecasting?

It connects Profit & Loss, Cash Flow, and Balance Sheet movements, making financial information more consistent and easier to explain.

How can businesses improve confidence in their financial information?

By building reliable management accounts, connected forecasting, and financial structures that produce consistent, decision-ready information.