When Is a Business Loan an “Engine” for Growth Versus an “Anchor” for Your Cash Flow?

A business loan becomes useful when the business can absorb the financial pressure operationally, not just when the growth opportunity looks attractive.

Many SMEs evaluate borrowing primarily through:

- revenue potential

- expansion plans

- hiring opportunities

- expected future growth

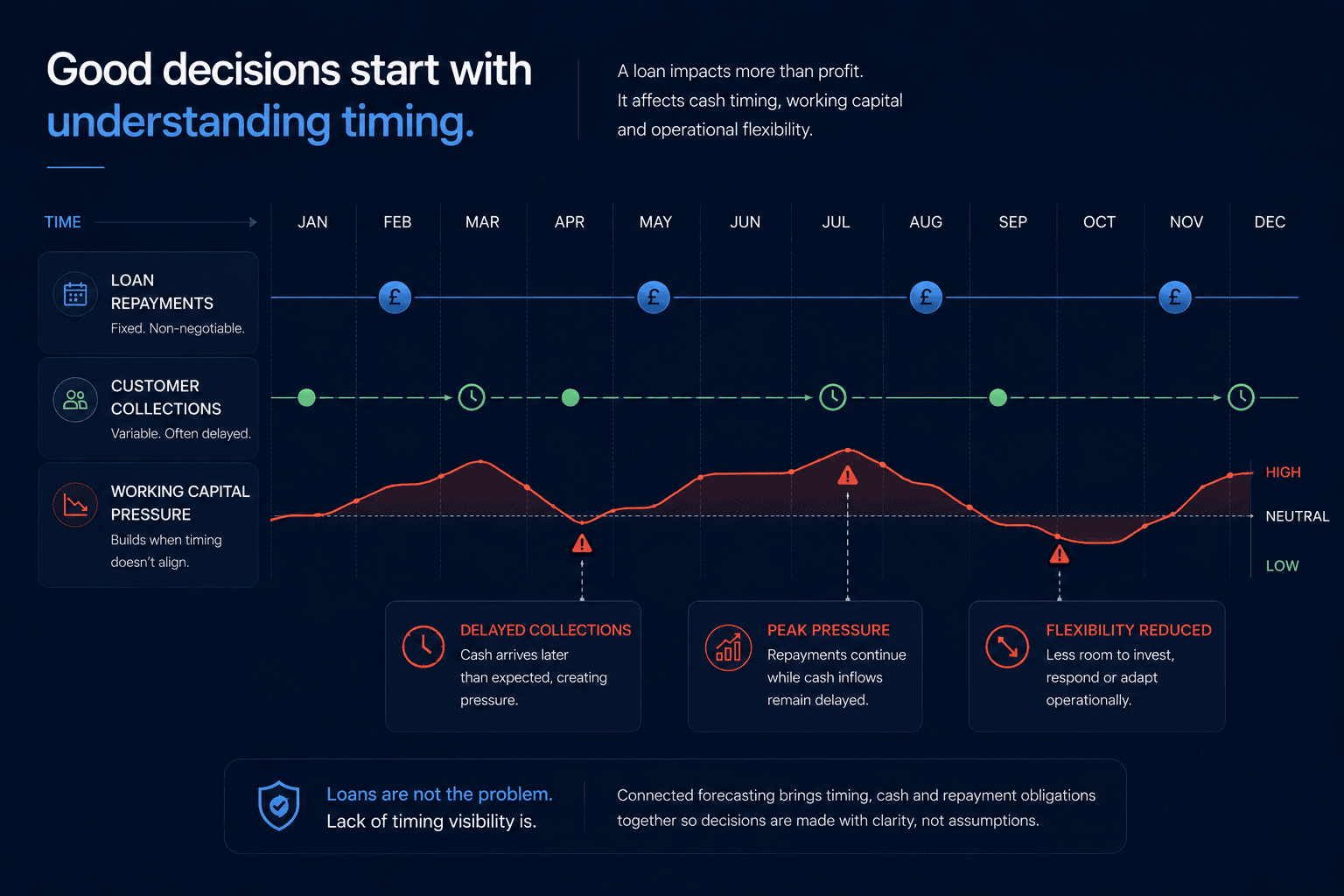

But loans affect much more than profit.

They also affect:

- cash timing

- working capital

- operational flexibility

- forecasting reliability

The difference between growth-supporting debt and cash flow pressure usually comes down to how well the business understands the financial behaviour underneath the borrowing.

Key Takeaways

- Borrowing is not inherently good or bad for SMEs

- Loans become risky when cash timing is poorly understood

- Revenue growth does not always translate into cash capacity

- Forecasting quality often determines whether borrowing remains sustainable

- 3-way forecasting improves visibility over borrowing impact

Why Borrowing Often Looks Simpler Than It Really Is

At first glance, many borrowing decisions appear relatively straightforward.

For example:

- additional revenue is expected

- new customers are forecast

- operational growth appears achievable

The loan, therefore, feels like a growth enabler.

And sometimes it is.

But what businesses often underestimate is how borrowing can alter financial behaviour beneath the surface.

Because growth itself usually creates additional pressure around:

- working capital

- cash conversion timing

- operational costs

- repayment obligations

The loan may support growth operationally while simultaneously creating strain elsewhere in the business.

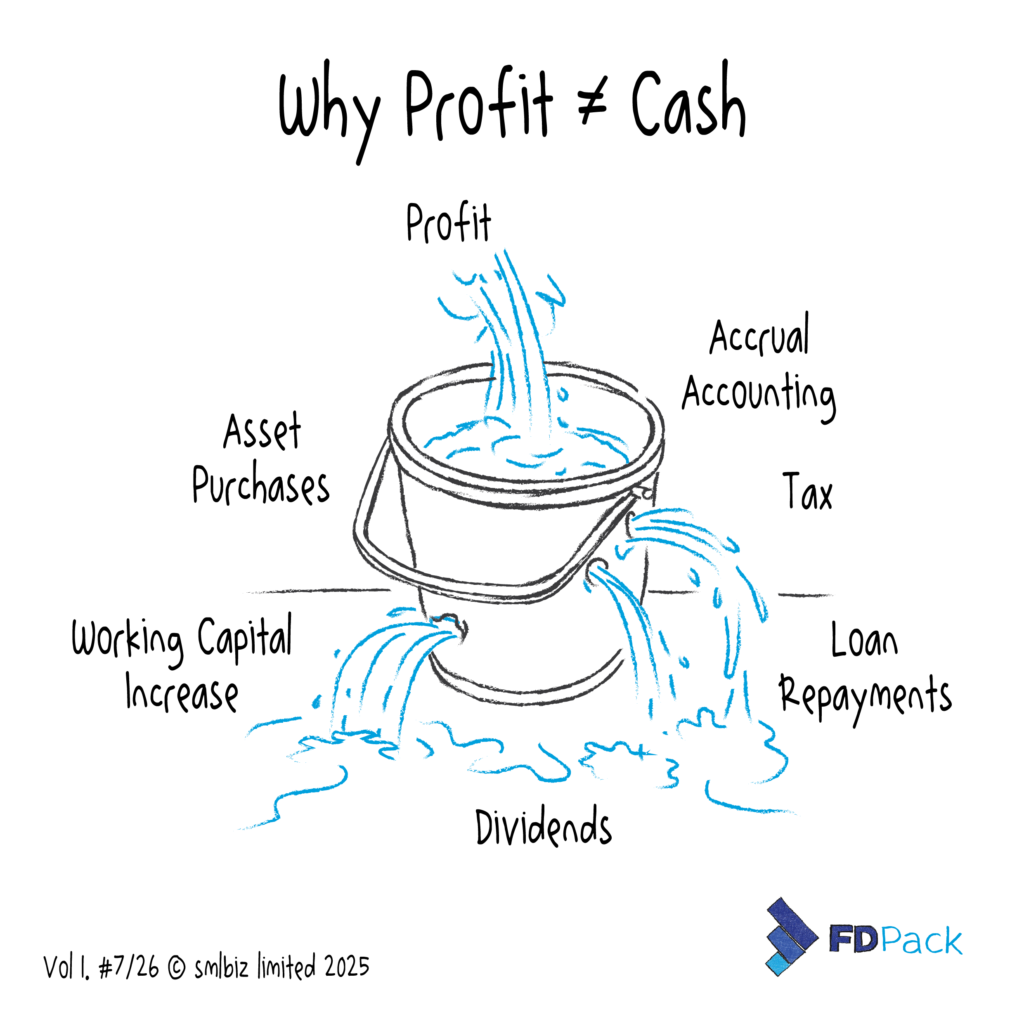

Why Revenue Growth Does Not Always Improve Cash Flow

One of the most common mistakes in SME forecasting is assuming: stronger revenue automatically creates stronger cash flow.

In reality, growth often increases financial pressure before cash benefits fully materialise.

For example:

- larger projects may extend payment cycles

- hiring costs often arrive before revenue converts to cash

- inventory or delivery costs may increase upfront

- repayments continue regardless of operational timing changes

This is why timing matters. Research from the British Business Bank found that 46% of SMEs apply for finance a week before needing it, or after it is already needed. That suggests borrowing is often reactive rather than planned around operational cash behaviour.

The risk is not always the loan itself.

It is taking on finance before the timing has been properly understood.

At smaller scale, these pressures may remain manageable. As borrowing increases, timing becomes much more important.

Profitability and liquidity do not always move together.

Why Cash Timing Usually Determines Whether Debt Feels Sustainable

Many businesses do not struggle because the loan itself was inappropriate.

They struggle because the timing behaviour around the loan was not fully understood operationally.

This often appears through:

- delayed customer payments

- seasonal cash fluctuations

- rising working capital requirements

- repayment schedules disconnected from operational cash flow

Initially, growth may still appear positive on paper.

But underneath:

- cash flexibility tightens

- forecasting becomes harder to maintain

- operational decisions become more reactive

This is often the point where borrowing starts behaving more like an anchor than an engine.

How the Same Loan Can Produce Different Outcomes

The difference is usually not the loan product itself.

It is the visibility around how the business absorbs the debt operationally.

| Borrowing Without Connected Forecasting | Borrowing With Connected Financial Visibility |

| Revenue growth viewed in isolation | Growth linked to cash and balance sheet impact |

| Loan affordability based mainly on profit | Repayments assessed against operational cash timing |

| Forecasts updated manually | Financial movements remain connected |

| Cash pressure appears reactively | Timing pressure becomes visible earlier |

| Operational growth creates unexpected strain | Growth assumptions tested operationally |

| Decisions rely heavily on optimism | Decisions supported by connected forecasting |

Borrowing becomes more reliable when financial behaviour remains visible across the whole business.

Why Forecasting Matters More Than Optimism

Growth assumptions are often optimistic by nature.

That is not necessarily a problem.

The issue is when optimism is unsupported by connected financial forecasting.

For example:

- revenue forecasts may increase while cash conversion slows

or:

- operational expansion accelerates while repayment pressure compounds underneath

This caution around borrowing is reflected more broadly across UK SMEs. Research from DJS Research found that only 43% of SMEs have recently used external finance such as loans, overdrafts, or credit facilities, often because businesses remain uncertain about managing repayment pressure and future cash flow reliably.

This is why forecasting quality matters so much in borrowing decisions.

Not because forecasting predicts the future perfectly.

But because it allows businesses to understand how financial movements interact over time. A forecast is only useful if it behaves like the business itself.

How 3-Way Forecasting Improves Borrowing Decisions

One of the biggest weaknesses in SME borrowing decisions is disconnected financial modelling.

Businesses often forecast revenue, and sometimes profit, while cash flow and balance sheet movements are reviewed separately later.

Connected 3-way forecasting improves visibility by linking:

- profit

- cash flow

- and balance sheet behaviour together

This allows businesses to see:

- how repayments affect liquidity

- how growth changes working capital requirements

- whether operational cash generation can realistically support the debt over time

The objective is not heavier forecasting. It is understanding how borrowing behaves operationally before pressure emerges.

As borrowing complexity increases, businesses often respond by adding more spreadsheets, assumptions, and scenario layers.

The problem is often too much financial weight and not enough clarity underneath it.

In practice, borrowing decisions usually become more reliable when the financial structure underneath them is simpler, more connected, and easier to interpret operationally over time.

What Better Borrowing Visibility Actually Looks Like

Reliable financial visibility around borrowing usually includes:

- forecasting connected directly to actual performance

- visibility over cash timing and liquidity

- understanding of operational working capital pressure

- financial structures that remain usable as growth accelerates

This allows businesses to make borrowing decisions with:

- greater confidence

- less reactive cash management

- and better operational visibility over future pressure points.

Borrowing Works Best When Financial Behaviour Stays Visible

Borrowing becomes dangerous less because of the debt itself and more because businesses lose visibility over how the financial pressure behaves operationally over time.

As SMEs scale, growth decisions increasingly affect:

- cash timing

- liquidity

- operational flexibility

- and forecasting reliability simultaneously.

FDPack helps growing SMEs build connected forecasting and financial reporting structures that improve visibility over how borrowing affects the wider business, allowing growth decisions to be tested operationally before financial pressure becomes difficult to manage.

Because the strongest borrowing decisions are rarely driven by optimism alone.

They are supported by financial information that continues to behave reliably as the business grows.

FAQs

Why can profitable businesses still struggle with loan repayments?

Because profitability and cash flow do not always move together, particularly when growth increases working capital pressure.

What makes borrowing risky for growing SMEs?

Poor visibility over cash timing, repayment pressure, and operational financial behaviour often creates borrowing risk.

Why does growth sometimes create cash flow pressure?

Because operational expansion often increases upfront costs and working capital requirements before revenue converts into cash.

How does connected forecasting improve borrowing decisions?

It allows businesses to understand how profit, cash flow, and balance sheet movements interact as borrowing affects the wider business.

Why is forecasting important before taking on debt?

Because it helps businesses understand whether future cash generation can realistically support repayments as operational complexity increases.