What the First 90 Days of Fixing Your Finance Function Look Like

Most finance functions do not break all at once.

Problems usually build gradually through:

- disconnected spreadsheets

- delayed reporting

- unreliable forecasts

- inconsistent management information

- and financial processes that no longer reflect how the business actually operates

Over time, businesses often compensate manually.

- Someone explains the numbers.

- Adjusts reports.

- Rebuilds forecasts.

- Reconciles differences between systems.

Eventually, the finance function continues operating mainly through intervention rather than structure.

The first 90 days of fixing a finance function are therefore rarely about introducing more reporting.

They are usually about rebuilding reliability underneath the numbers.

Key Takeaways

- Most finance function problems develop gradually as businesses scale

- Manual workarounds often hide deeper structural issues

- Reliable reporting depends on connected financial information

- Forecasting becomes difficult when financial systems evolve separately

- The first 90 days usually focus on rebuilding visibility and consistency

- Better finance functions improve operational decision-making, not just reporting speed

Why Do Finance Functions Usually Start Breaking During Growth?

In smaller businesses, finance processes often evolve reactively.

New reports get added.

Additional spreadsheets appear.

Forecasts are adjusted manually.

Operational processes change faster than financial structures.

Initially, this works reasonably well.

But as businesses grow, complexity increases faster than the finance function is able to adapt and grow to manage it.

This often creates:

- duplicated reporting

- inconsistent assumptions

- disconnected forecasts

- reporting delays

- reduced confidence in the numbers

The issue is rarely one major failure.

It is usually the gradual accumulation of small financial disconnects over time.

Research from the Association of Chartered Certified Accountants, based on over 10,000 SME interviews, found that financial capability is not simply a result of business growth, but one of its causes.

As businesses scale, weak finance structures often become visible operationally long before they are addressed structurally.

What Are the Early Signs That a Finance Function Needs Fixing?

Most businesses notice the symptoms operationally before identifying the underlying structural problem.

For example:

- management accounts take longer to produce

- forecasts require increasing manual adjustment

- cash visibility weakens

- different reports show different versions of performance

- operational teams lose confidence in financial reporting

At this stage, the business often still functions commercially.

But financial visibility becomes increasingly dependent on manual interpretation.

Research published by the UK Government found that only 46% of UK businesses handling digital data agreed that data analysis or processing supports their business decisions, highlighting how many organisations still struggle to convert reporting into operational visibility.

Having more reports does not automatically create more reliable decision-making.

Why Do Forecasts Usually Become Unreliable First?

Forecasting is often where financial problems become most visible.

Because forecasts depend on:

- reliable actuals

- consistent assumptions

- connected reporting structures

- and operational timing behaves predictably

When finance systems evolve separately, forecasts gradually lose reliability.

For example:

- sales forecasts may disconnect from cash timing

- hiring assumptions may not flow through operational costs correctly

- working capital movements may be reviewed retrospectively instead of dynamically

This creates forecasts that technically update, but no longer fully reflect how the business behaves operationally.

- The issue is not forecasting itself.

- It is the reliability of the underlying financial structure.

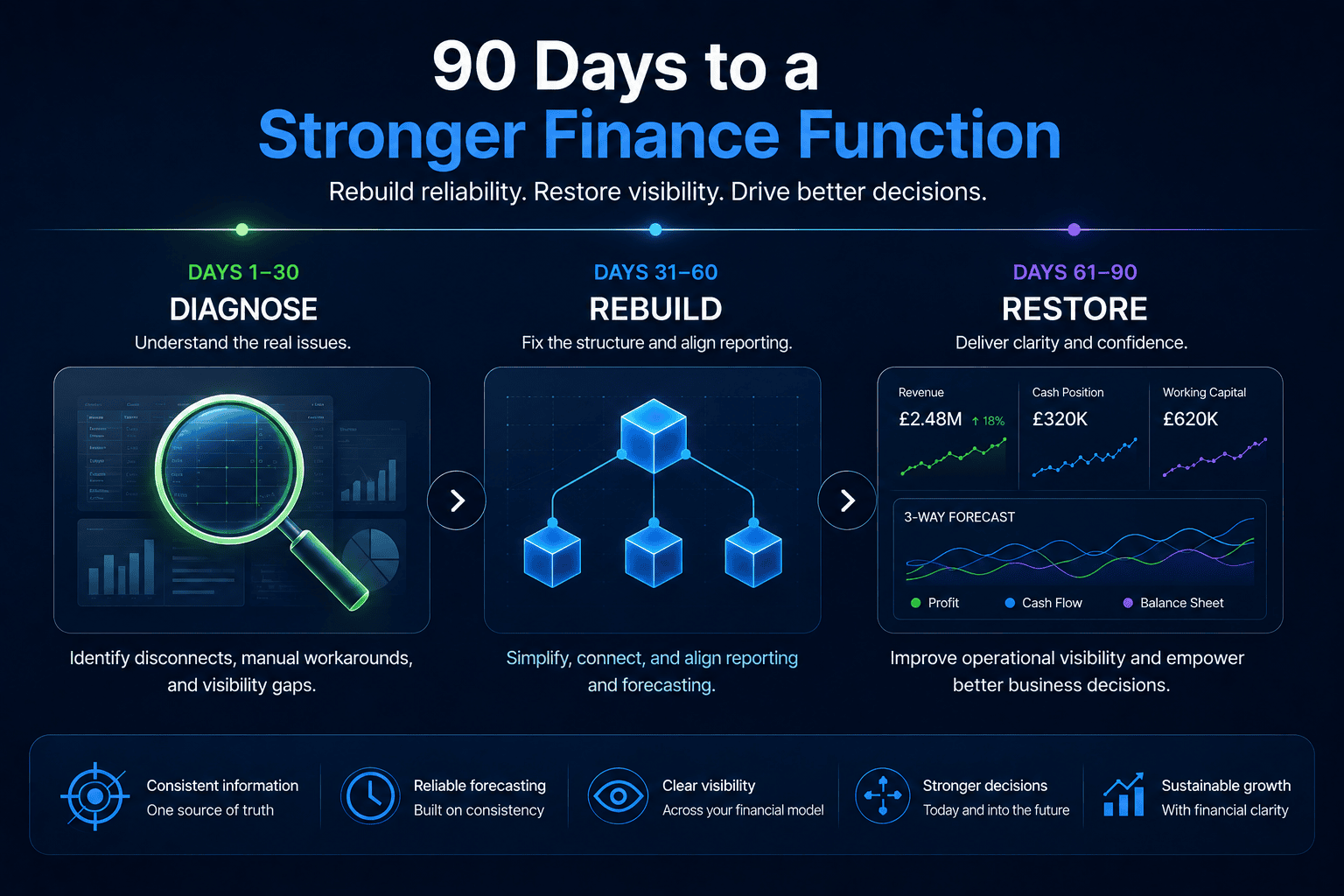

What Actually Happens During the First 30 Days?

The first stage is usually diagnostic rather than transformational.

The objective is to understand:

- where reporting disconnects exist

- how operational data flows through the business

- where manual intervention is compensating for weak structure

- and which areas are creating the greatest visibility problems

This often includes reviewing:

- management accounts

- forecasting models

- reporting timelines

- chart of accounts structures

- cash flow visibility

- operational reporting dependencies

At this stage, businesses are often surprised by how much of the finance function depends on:

- manual reconciliation

- spreadsheet workarounds

- and operational assumptions held outside the reporting structure itself.

What Changes During the Second 30 Days?

Once the underlying issues become visible, the next phase usually focuses on rebuilding consistency.

This often includes:

- simplifying reporting structures

- aligning management accounts with operational activity

- improving forecasting logic

- reducing duplicated assumptions across spreadsheets

- reconnecting financial information across reporting areas

The objective is not to create more reporting.

It is to create reporting that behaves consistently over time.

| Before Finance Function Cleanup | After Financial Structures Become Connected |

| Forecasts updated manually | Forecast assumptions remain aligned |

| Reporting delays increase | Management information becomes more consistent |

| Different spreadsheets evolve separately | Financial structures become connected |

| Cash visibility weakens | Liquidity movements become easier to track |

| Operational decisions rely on interpretation | Reporting becomes more usable operationally |

Reliability usually improves when the financial structure becomes simpler and more connected underneath.

What Happens During the Final 30 Days?

Once reporting consistency improves, the focus usually shifts toward operational visibility.

This means ensuring the finance function can support:

- decision-making

- forecasting

- growth planning

- and cash visibility is reliably going forward.

Connected 3-way forecasting often becomes particularly important here because it links:

- profit

- cash flow

- and balance sheet behaviour together

This helps businesses understand how operational changes affect the wider financial position over time.

Rather than reviewing financial movements separately after problems emerge, the business gains earlier visibility over:

- liquidity pressure

- working capital changes

- operational timing strain

- and forecasting drift.

Why Do Businesses Often Overcomplicate Finance Transformation Projects?

Many businesses assume finance transformation requires:

- heavier systems

- more dashboards

- additional reporting layers

- or increasingly complex forecasting models

But complexity rarely improves financial visibility on its own.

In practice, finance functions usually improve when:

- assumptions become more consistent

- reporting structures remain connected

- operational data flows more cleanly

- and forecasting reflects how the business actually behaves over time.

The objective is not more reporting.

It is creating financial information that becomes easier to trust operationally.

Better Finance Functions Depend on Reliability, Not More Reporting

The first 90 days of fixing a finance function are rarely about introducing dramatic change.

They are usually about rebuilding consistency underneath the numbers.

As businesses grow, financial reporting often becomes increasingly fragmented through manual adjustments, disconnected forecasting, and operational workarounds.

FDPack helps growing SMEs rebuild connected reporting and forecasting structures that improve financial visibility as operational complexity increases.

Because the strongest finance functions are not necessarily the most complicated.

They are the ones that continue producing reliable financial information as the business evolves.

FAQs

Why do finance functions become unreliable as businesses grow?

Because operational complexity often increases faster than reporting structures, forecasting processes, and financial systems evolve underneath.

What are the signs that a finance function needs fixing?

Delayed reporting, inconsistent forecasts, weak cash visibility, and increasing manual reconciliation are common warning signs.

Why does forecasting usually break first?

Because forecasting depends on reliable actuals, connected reporting structures, and operational assumptions remaining aligned over time.

What happens during a finance function transformation?

Businesses typically simplify reporting structures, improve forecasting consistency, reconnect financial information, and strengthen operational visibility.

How does connected forecasting improve financial visibility?

It links profit, cash flow, and balance sheet behaviour together so businesses can understand how operational decisions affect the wider financial position.