Statutory Profit vs EBITDA: Why the Numbers Don’t Tell the Same Story

Statutory profit and EBITDA are not competing metrics.

They answer different questions.

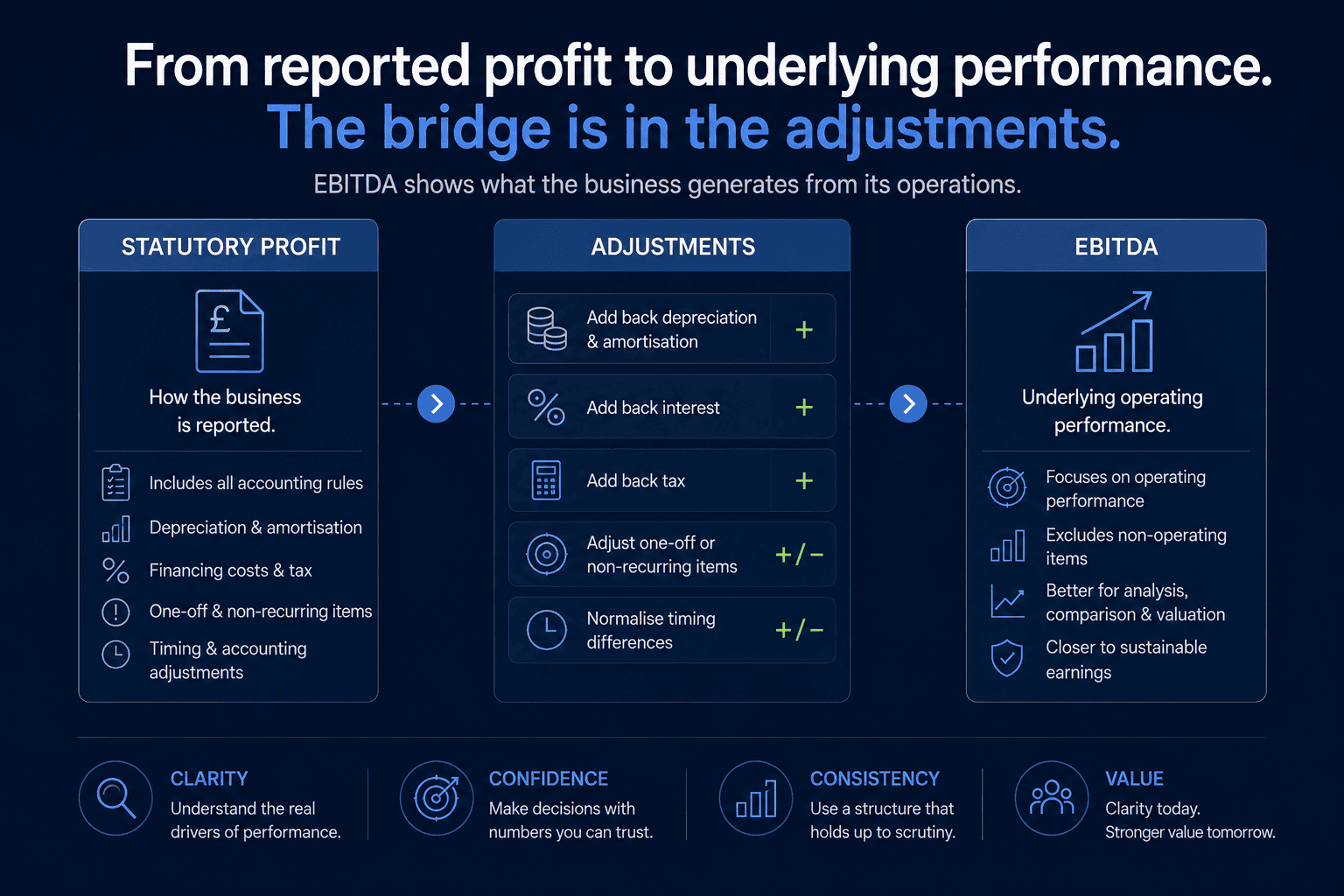

- Statutory profit reflects how the business is reported

- EBITDA is used to understand the underlying performance

The gap between them is where interpretation becomes important.

If that gap is not understood, decisions are made on numbers that do not reflect how the business actually operates.

Key Takeaways

- Statutory profit is shaped by accounting rules and timing

- EBITDA focuses on the underlying operating performance

- The difference between them is often misunderstood

- Buyers and investors rarely rely on statutory profit alone

- Adjustments need to be consistent and justifiable

- Clarity improves confidence, which affects valuation

Why Statutory Profit Doesn’t Always Reflect Performance

Statutory profit is designed for compliance.

It includes:

- depreciation and amortisation

- financing costs

- tax

- accounting adjustments

- one-off or non-recurring items

These are necessary for reporting.

But they do not always reflect:

- how the business is performing day-to-day

- what is sustainable

- what can be expected going forward

The number is correct.

But it is not always useful for decision-making.

What EBITDA Is Trying to Show

EBITDA removes:

- interest

- tax

- depreciation

- amortisation

The intention is to isolate: operating performance before structural and accounting effects.

It helps answer:

- what does the business generate from its operations?

- how does performance compare across periods?

EBITDA is not a complete answer. It is a starting point, not a conclusion.

Where the Gap Comes From

The difference between statutory profit and EBITDA typically comes from:

- non-cash expenses (depreciation, amortisation)

- financing structure

- tax treatment

- one-off or exceptional items

- timing differences

This gap is not unusual. But it needs to be understood.

These differences affect how profit, cash, and financial position move over time.

To understand the full impact, these adjustments must also be reflected in cash flow and the balance sheet.

Otherwise, the model shows performance, but not how the business actually behaves.

How the Same Business Can Look Different

The impact of these differences becomes clearer when comparing how the same business is viewed under each metric.

| Area | Statutory Profit View | EBITDA View |

| Focus | Compliance and reporting | Operating performance |

| Includes | All accounting charges | Excludes non-operating items |

| Treatment of one-offs | Included | Often adjusted out |

| Comparability | Limited across periods | Easier to compare performance |

| Use case | Reporting and tax | Analysis and valuation |

| Decision relevance | Can be limited | More aligned with operational decisions |

The difference is not “accuracy”. It is “purpose”.

Why Buyers Don’t Rely on Statutory Profit

When assessing a business, buyers want to understand:

- sustainable earnings

- risk

- future performance

Statutory profit includes too much noise to answer these questions on its own.

Instead, buyers:

- adjust for one-off items

- normalise costs

- isolate recurring performance

The objective is to understand what the business actually generates.

What “Normalised” Actually Means

Normalisation is not about changing the numbers.

It is about:

- removing distortions

- isolating recurring activity

- making performance comparable

Common adjustments include:

- owner or non-market salaries

- one-off legal or restructuring costs

- non-recurring income

- unusual accounting entries

The goal is clarity, not manipulation.

Where This Goes Wrong

Problems arise when:

- adjustments are inconsistent

- assumptions are not explained

- numbers are presented without context

This leads to:

- loss of credibility

- difficulty during due diligence

- reduced confidence from buyers

The issue is not the adjustment.

It is how it is applied.

If the adjustments aren’t clear, the numbers won’t be trusted.

Without a structured model, this gap continues to create confusion rather than insight.

Why Structure Matters More Than Adjustments

Adjustments can improve clarity.

The problem is not a lack of adjustment. It is too much weight and not enough clarity.

But if the underlying structure is weak:

- issues continue to reappear

- reporting remains inconsistent

- forecasts become unreliable

A stronger approach is:

- consistent categorisation

- clear separation of recurring vs non-recurring

- alignment between reporting and forecasting

This reduces the need for repeated adjustments.

How This Supports Better Decisions

When financial data reflects underlying performance:

- trends are clearer

- assumptions are easier to test

- decisions can be made more confidently

This affects:

- investment decisions

- hiring plans

- pricing strategies

- growth planning

The value is not in producing adjusted numbers.

It is in understanding what drives them.

This also allows performance to be projected more reliably, not just explained historically.

The Difference Is Where the Insight Sits

Statutory profit and EBITDA are both valid.

But they serve different purposes.

The gap between them is where:

- performance is interpreted

- adjustments are made

- decisions are shaped

Understanding that gap is critical.

Because that is where:

- clarity is created

- confidence is built

- value is determined

If your current financial reporting does not clearly distinguish between reported profit and underlying performance, it may limit both decision-making and valuation outcomes.

FD Pack combines:

- senior financial expertise

- structured, expert-led financial systems built around how the business operates

to deliver:

- clear, consistent management accounts

- forward-looking financial insight

This provides:

- clarity

- confidence

- and numbers that support decisions.

This ensures the numbers are not just accurate, but decision-ready.

FAQs

What is the difference between statutory profit and EBITDA?

Statutory profit includes all accounting items, while EBITDA focuses on operating performance by excluding interest, tax, and non-cash charges.

Why do investors focus on EBITDA?

Because it helps assess underlying performance and compare businesses more consistently.

What is normalised EBITDA?

It is EBITDA adjusted for one-off or non-recurring items to reflect sustainable earnings.

Is EBITDA always better than statutory profit?

No. Both are useful, but they serve different purposes.

Why does this matter for valuation?

Because valuation depends on sustainable earnings, not just reported profit.