How Clean Finance Forecasting Increases Your Final Exit Multiple

Valuation is driven by how well a buyer can rely on your financial model.

A forecast that:

- aligns with actual performance

- reflects how cash behaves

- explains financial position

can be tested.

If a forecast cannot be tested, it cannot be relied on.

And if it cannot be relied on, it reduces confidence in the outcome.

Key Takeaways

- Buyers assess how the model behaves, not just what it shows

- Forecasts must extend directly from actual financial data

- Profit, cash, and position must be connected

- Disconnected models reduce confidence

- Structure determines reliability

- Predictability supports stronger valuation outcomes

Why Valuation Is Driven By Confidence, Not Just Performance

Valuation increases when a buyer can clearly understand and rely on your financial model.

At exit, buyers are not only reviewing results.

They are assessing:

- how those results are generated

- how cash flows through the business

- how consistent performance is likely to be

Two businesses with similar performance can be valued differently.

The difference is often: how clearly the financial model can be understood and relied upon.

This is reflected in transaction outcomes. Research from Harvard Business Review suggests that 70–90% of M&A deals fail to achieve their intended value, often due to issues identified during diligence.

Where Forecasting Typically Breaks Down

Forecasting breaks down when it is disconnected from actual financial data

In many businesses, forecasting is treated as a separate exercise.

- historical accounts sit in one place

- forecasts sit in another

- assumptions are applied at a high level

This leads to:

- inconsistencies between reports

- limited visibility of cash timing

- difficulty explaining movements

The issue is not the forecast itself. It is the absence of a consistent underlying structure.

Why Buyers Test How Your Forecast Behaves, Not Just What It Shows

A forecast is not assessed on presentation.

It is assessed on whether it reflects how the business actually operates.

For example:

- a sale increases revenue

- that creates a receivable

- which converts into cash over time

If a forecast only shows the first step, it is incomplete.

If it shows the full flow, it can be tested.

This is how buyers assess reliability.

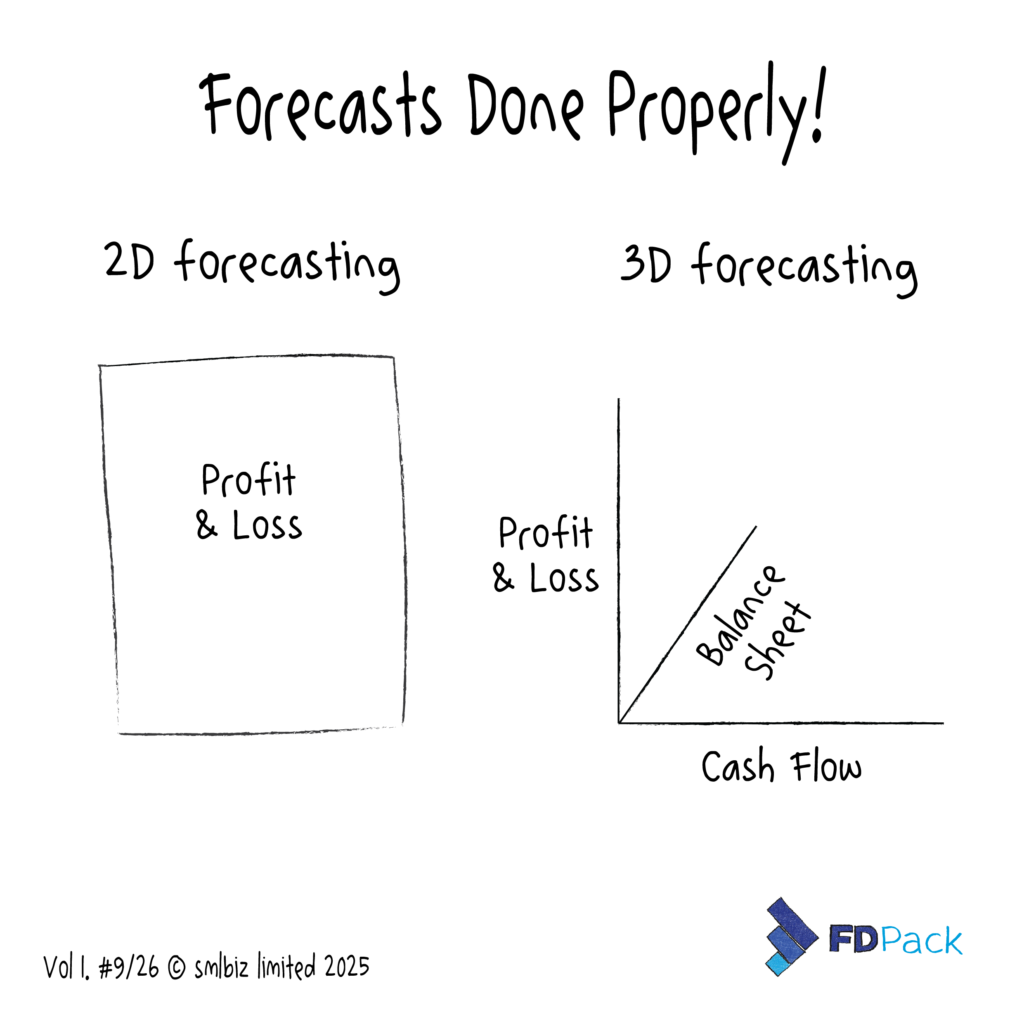

Why 3 – Way Forecasting Is Central To Valuation

A reliable 3-way forecasting model connects:

- Profit & Loss → performance

- Cash Flow → movement of cash

- Balance Sheet → financial position

Each transaction:

- impacts more than one area

- flows through the model

- can be traced and explained

This is what allows the model to hold together.

These movements occur over time, not at once.

A model that reflects this timing behaves like the business.

Without this:

- cash behaviour is unclear

- movements cannot be reconciled

- projections are difficult to rely on

Why The Forecast Must Extend Directly From Actuals

A forecast should not exist as a separate model.

It should be a continuation of the same structure.

At any point:

- past periods are actual

- future periods are forecast

But structurally, they are part of one model.

When this is not the case:

- differences emerge

- reconciliation becomes difficult

- confidence is reduced

Buyers will test this alignment directly.

Why Timing and Revenue Recognition Must Be Reflected Correctly

A forecast must reflect how transactions behave in practice.

For example:

- SaaS businesses often receive cash in advance

- revenue is recognised over time

- the balance sits as deferred income

If this is not handled correctly:

- profit may appear overstated

- cash may appear disconnected

- forecasts may not align with reality

This is not a reporting issue. It is a modelling issue.

Why Financial Complexity Often Increases As Businesses Grow

As businesses scale, finance systems often become:

- more detailed

- more fragmented

- less consistent

This typically involves:

- additional reports

- separate models

- overlapping assumptions

More information is produced, but clarity is reduced.

Many businesses respond by adding more models, more reports, and more layers.

The problem is not a lack of detail. It is too much weight and not enough clarity.

The Importance Of Simplifying The Model Before Improving It

A structured approach focuses on:

- a single financial model

- consistent logic across all periods

- removal of unnecessary complexity

The objective is:

- fewer moving parts

- clearer relationships

- more reliable outputs

Simplicity improves usability. Structure ensures the model holds together.

How This Gets Exposed in a Transaction

If your forecast:

- sits separately from your reporting

- does not explain cash movements

- cannot be easily reconciled

then it is likely to be tested heavily in a transaction.

At this stage, the focus should be on:

- structure

- consistency

- clarity

Not additional reporting.

Valuation Follows Model Integrity

Valuation is not determined solely by growth.

It is influenced by:

- how clearly performance can be understood

- how reliably future outcomes can be assessed

A model that:

- connects profit, cash, and position

- extends from actual data

- reflects how the business operates

provides a stronger basis for decision-making.

Model integrity supports confidence. Confidence supports valuation.

If your current forecasting model does not reflect how profit, cash, and position interact, it is likely to be tested in detail during a transaction.

FDPack combines:

- senior financial expertise

- structured, purpose-built forecasting systems

to deliver:

- integrated management accounts

- rolling forecasts that extend directly from actuals

All are built on a consistent 3-way model.

This provides:

- clarity

- consistency

- and financial information that can be relied on in a transaction context.

If your forecast doesn’t reflect reality, it won’t survive scrutiny.

FAQs

1. Why does clean forecasting affect valuation?

Because it improves how reliably future performance can be assessed. Clear, structured models reduce uncertainty.

2. What is meant by a forecast that “holds together”?

It means all financial movements are connected and consistent. Outputs can be explained and reconciled.

3. Why is 3-way forecasting important at exit?

It connects profit, cash, and financial position. This allows buyers to test and rely on the model.

4. What is the biggest forecasting issue during a sale?

Disconnected models that do not align with actual data. This reduces confidence and increases scrutiny.

5. What should a forecasting model include?

A single, integrated structure linking P&L, cash flow, and balance sheet. Built as a continuation of actual financial data.